News

Private Health Insurance sure can feel like it takes a big chunk out of household budgets, and with the annual premium hike each year, it’s little wonder it can sometimes be the first thing to get the chop when trying to cut back. But before you pull the plug make sure you are fully aware of the potential tax consequences!

For example; depending on your income level, the savings you make after cutting it may be completely wiped out with the extra tax you’ll be forking out at tax time.

The Medicare Levy is a tax we all need to pay, with each of us contributing 2% of our taxable income (with some exceptions) to fundMedicare. This is the backbone of Australia’s top notch public health care system… A very worthy cause indeed. This is different, however, to the MedicareLevy Surcharge, or MLS or short.

The MLS was designed to encourage people to take out private patient hospital cover and use the private hospital system to reduce demand on the public Medicare system. It is an additional tax you must pay if you earn over a certain threshold and do not have the “appropriate level of cover” (more on this below!)

The total amount of MLS you will need to pay is dependent on your income for MLS purposes. So, this isn’t just what your employer pays you, but it includes any fringe benefits and the net amount on which family trust distribution tax has been paid.

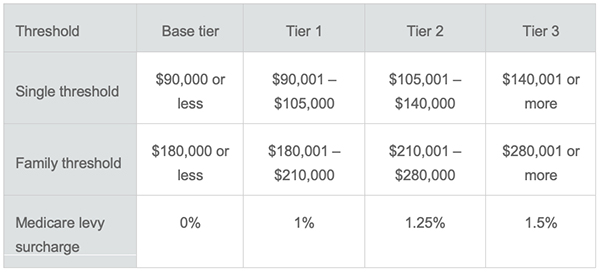

The MLS is calculated on two income thresholds – single and family – and increases across four income tiers. You are in MLS territory when a single person earns more than $90,000 or a family’s combined taxable income is more than $180,000. For families who have two or more dependent children, the family income threshold is increased by $1,500 each after the first one.The ATO provides this handy little table which might explain it a little easier:

If you or your family are in these income tiers and you don’t have appropriate level of private health cover, you will be up for MLS when you lodge your tax return. If you wish to avoid this extra tax and don’t mind spending a little extra on your health insurance, then the next step is to get yourself an eligible health insurance policy.

• Days held: If you’ve only held hospital cover for only part of the tax year, then you’ll only have a partial exemption from the MLS. This means you’ll have to pay the surcharge for all the days you did not have private hospital cover.

• If you are a family (and this also means a de-facto relationship), you will need appropriate cover for the entire family. This includes you, your partner and any children. If you don’t include your children in your cover, you will not be appropriately covered for the days in which they are not under your policy. This means you’re up for the MLS even though you maybe paying for a full policy for yourself!

• Not all private health insurance policies are equal, or indeed eligible. The ATO only accepts policies for ‘hospital cover ’or ‘combined hospital and extras cover’. This means you cannot sign up for just ‘extras’ or ‘general treatment’ and still avoid the MLS. Be sure to shop around and ensure the policy you choose is appropriate and will keep you out of theMLS territory.

If you’d like help or advice managing your tax situation –from the MLS and beyond – speak with the Attune team today. Call 1300 866 113or click here to start the conversation on email.